The Market Has Learned to Read

For decades, financial markets ran on a simple idea: the fastest data and sharpest math would win. So quant firms spent billions on proximity servers, fast execution engines, and secret factor models. But something began to shift around 2023. By 2026, that shift has become a structural change in how global capital moves.

“The goal of forecasting is not to predict the future but to tell you what you need to know to take meaningful action in the present.”

— Paul Saffo, Futurist and Technology Forecaster

How LLMs Entered Finance

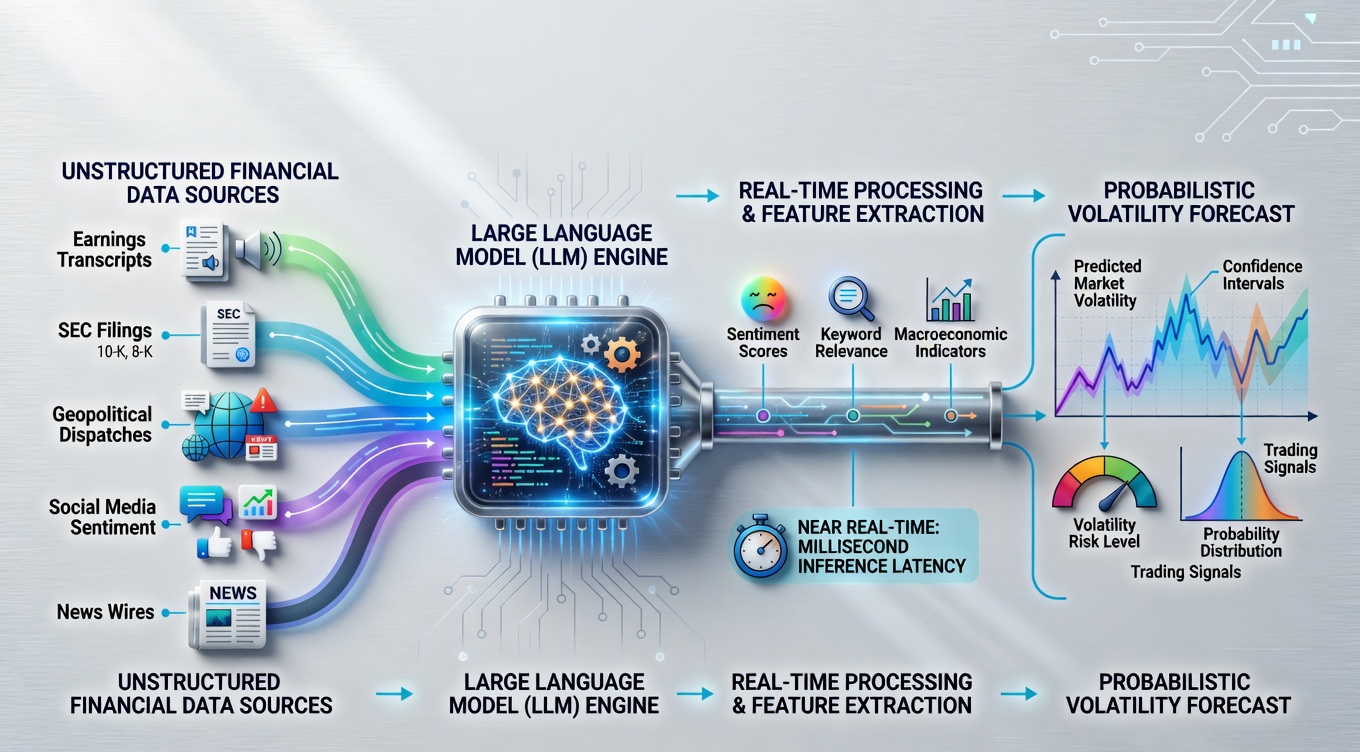

Furthermore, Large language models (LLMs) — the same AI behind chatbots — have moved into quantitative finance. They are not just research tools anymore. Instead, they now run inside trading algorithms. Moreover, they read earnings call transcripts, Fed minutes, geopolitical risk reports, and social media sentiment in real time.

As a result, “market data” now includes more than just price and volume. It includes almost anything expressed in language.

Thus, this article looks at how LLMs are reshaping algorithmic trading in 2026. Therefore, we focus on predicting volatility in the tech sector. We also explore regulation, risks, and future paths for engineers, portfolio managers, and policymakers.

From Rule-Based Algorithms to Neural Intuition

However, to understand today’s revolution, you first need to know where algorithmic trading began. Early systems from the 1970s–1990s used hand‑coded rules. For example, a simple momentum strategy might buy a stock when its 50‑day average crossed above the 200‑day average.

These rules were clear, easy to check, and simple to explain to regulators. But they were also rigid. They could not adapt to market crashes or new conditions.

“An algorithm must be seen to be believed, and before it can be seen, it must first be written.”

—Donald Knuth, Computer Scientist and Author of ‘The Art of Computer Programming’

The next wave (2010–2022) brought machine learning: boosted trees, neural networks, and reinforcement learning. These models could spot non‑linear patterns that humans missed. Still, they mostly worked on structured data — numbers, prices, volumes. Language remained largely unused.

The Transformer Breakthrough

The arrival of transformer models — like GPT‑4o, Claude 3 Opus, Gemini Ultra, and BloombergGPT — was a turning point. These systems can reason about context, extract sentiment, find cause‑and‑effect in text, and create synthetic scenarios for stress tests.

Research by Wu et al.

1

found that BloombergGPT beat general models on financial NLP tasks by 10–30%. It performed better at headline classification, name recognition, and earnings sentiment analysis.

By 2026, fine‑tuned LLMs trained on private data — like broker research, alternative data, and options flow — run live inside major hedge funds. The jump from back‑test to real‑time trading has been faster than most experts predicted.

How LLMs Decode Volatility Signals

What’s more, volatility in the tech sector has always come from many sources: earnings surprises, economic shifts, regulatory news, and waves of sentiment. Traditionally, quants used GARCH models or stochastic volatility frameworks. But these methods struggle when the main trigger is language — for example, a CEO’s vague comment on an earnings call or a surprise regulatory probe announced just before markets open.

“Volatility is not the enemy of the investor — ignorance is. Where others see chaos, the prepared mind sees structure.”

—Howard Marks, Co-founder of Oaktree Capital Management

The Prediction Pipeline

Modern LLM‑based volatility systems work in several steps:

-

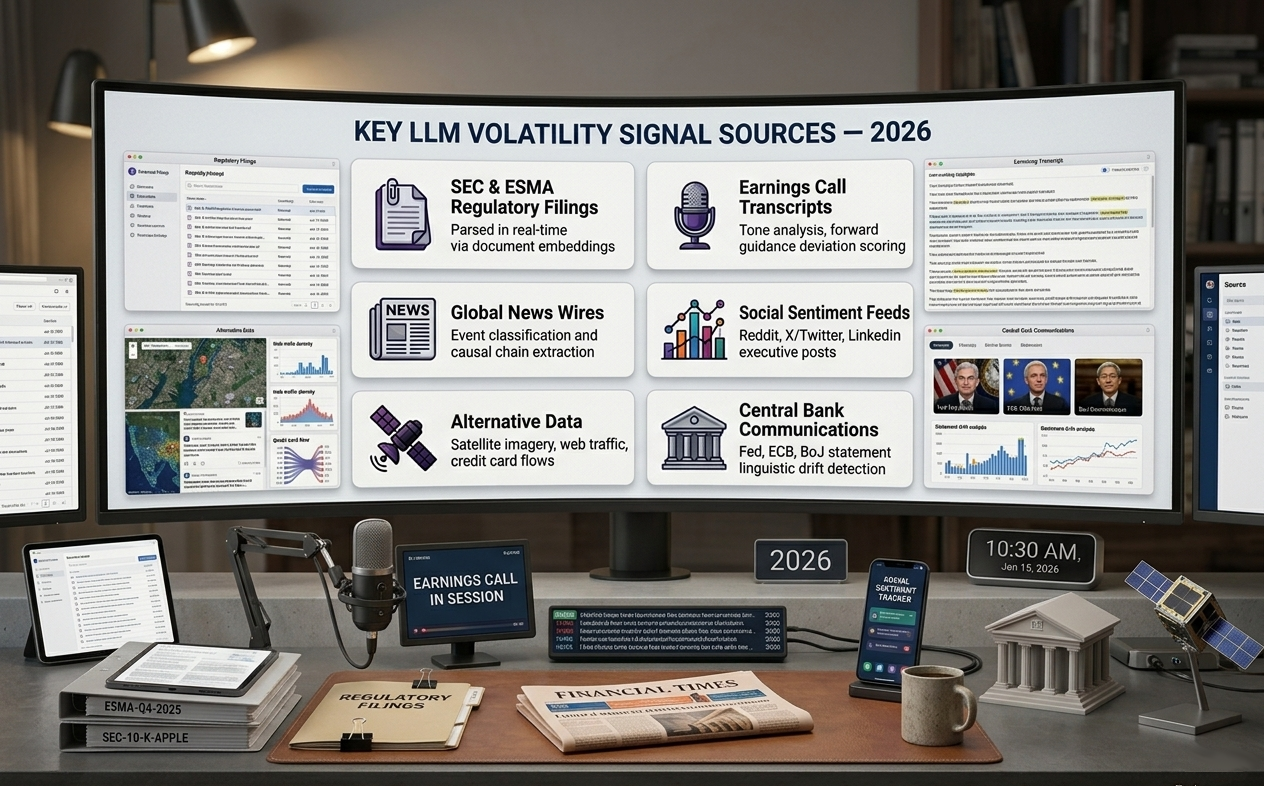

Real‑time ingestion – They pull from SEC EDGAR, ESMA, news wires, earnings call transcripts, and alternative data (like web traffic or satellite images).

-

Semantic encoding – A special embedding model turns each document into high‑dimensional vectors.

-

Probabilistic output – A fine‑tuned LLM decoder predicts the chance of high volatility over 1, 5, or 20 days.

A 2026 study by Zhang, Wang, and Chen

1

showed that transformer models beat traditional GARCH by 22.4% in mean absolute error for tech‑sector volatility. When combined with options flow data, the advantage grew to 31.7%.

Consider, for example, the case of a major cloud computing provider announcing unexpectedly weak guidance for the following quarter. Within 340 milliseconds of the transcript becoming available, LLM-driven systems at multiple firms had already classified the sentiment as materially bearish, identified three specific forward guidance phrases that deviated from prior quarter language, and initiated hedging positions in the options market — all before most human analysts had opened the document. This illustrates not merely speed, but semantic comprehension at scale.

A Real‑World Example

Imagine a major cloud provider announces weak guidance for next quarter. Within 340 milliseconds of the transcript appearing, LLM‑driven systems at several firms had already:

-

Classified the sentiment as very negative,

-

Found three forward‑guidance phrases that changed from the previous quarter,

-

And started hedging in the options market.

That is not just speed. It is real understanding of meaning at scale.

Risks, Regulation, and the Human Factor

Bringing LLMs into live trading brings new risks — both technical and systemic.

Technical Risks

LLMs can “hallucinate.” They may produce confident but wrong outputs. In trading, such errors can spread through automated systems before anyone checks them. A single misclassified earnings call could trigger a cascade of bad orders.

“The first principle is that you must not fool yourself — and you are the easiest person to fool.”

—Richard P. Feynman, Nobel Laureate in Physics

Systemic Risks

Regulators worry that if most big players use similar LLMs, all might react the same way to the same news. That could make volatility worse, not better. The Bank for International Settlements warned in November 2024

1

that “homogeneous AI adoption across financial institutions may reduce portfolio diversification at the systemic level.”

New Regulations

The EU’s Artificial Intelligence Act

1

— fully in force from August 2026 — labels high‑frequency AI trading systems as “high‑risk.” They must pass conformity checks, keep risk documents, and have human oversight.

In the US, the SEC’s Rule 15c3‑5

1

(Market Access Rule) now requires brokers to include AI‑generated order logic in pre‑trade risk controls. Also, the proposed Algorithmic Accountability Act [6] would require audit trails for any AI making major financial decisions.

Humans Still Matter

Apart from, despite these challenges, humans remain essential. The best firms are not removing people. Instead, they are redesigning their roles. Portfolio managers now act as “AI supervisors.” They check model confidence scores, challenge odd predictions, and override outputs when the model misses context that a human would catch. This human‑machine teamwork is the new gold standard for responsible AI in finance.

What Comes Next

Several trends will shape how LLMs evolve in trading systems.

Multimodal Models

New models can process text, audio, video, and numbers at the same time. By combining language with live prices and even chart patterns, they promise a much fuller view of the market.

“The measure of intelligence is the ability to change. Markets, like ecosystems, reward those who adapt — not those who are merely fast.”

— Charles Darwin (adapted)

Agentic AI

Autonomous LLM “agents” can now run multi‑step research, test hypotheses, and propose trades for human approval. A team that once needed ten researchers to develop one strategy can now run hundreds of parallel experiments.

Interpretability

Techniques like mechanistic interpretability and chain‑of‑thought auditing are opening the “black box.” It is becoming easier to explain why a model gave a certain volatility prediction. Regulators increasingly require this before approving a model for live use.

A JP Morgan report from January 2026

1

found that firms mixing LLM‑based signals with traditional quant factors achieved Sharpe ratios 18–34% higher than those using only AI or only quant methods. The future belongs to a disciplined mix of both.

Conclusion: Intelligence as Infrastructure

In 2026, algorithmic trading has reached a turning point. Large language models are no longer an experiment. They are core infrastructure for competing in markets. Their ability to interpret and act on language in milliseconds is a giant leap beyond older quant models.

But this power comes with responsibility. As LLMs grow stronger and more common, the risks of misalignment — between model behavior and market stability, between speed and regulation, between profit and safety — also grow. Engineers, financial firms, and regulators must work together to create frameworks that harness this intelligence without breaking what it touches.

“In the middle of every difficulty lies opportunity — but only for those disciplined enough to look beyond the volatility.”

— Albert Einstein (adapted)

The firms that lead the next decade will not just have the best models. They will be the ones that deploy AI responsibly — building systems that are faster, smarter, and also more transparent, more robust, and more aligned with healthy markets. The language of finance has always been data. In 2026, data has finally learned to speak — and the markets are listening.

References