Currently, by the first quarter of 2026, 92% of the Fortune 500 are paying ChatGPT customers. Furthermore, enterprise AI spending is projected to exceed $2.5 trillion. Additionally, more than 80% of large firms run AI agents in production environments. Yet, a troubling paradox dominates boardroom conversations. Specifically, productivity is soaring, while profit margins stall or even shrink.

Recently, the Boston Consulting Group Henderson Institute analyzed 800 U.S. public companies. Subsequently, their research revealed a surprising finding. Specifically, they found “no correlation between the resulting measure of gen AI automation potential per sector and the development of sector-level profit margins since the launch of ChatGPT.” In fact, the sectors with the highest automation potential—finance, technology, and media—saw margins stagnate or fall.

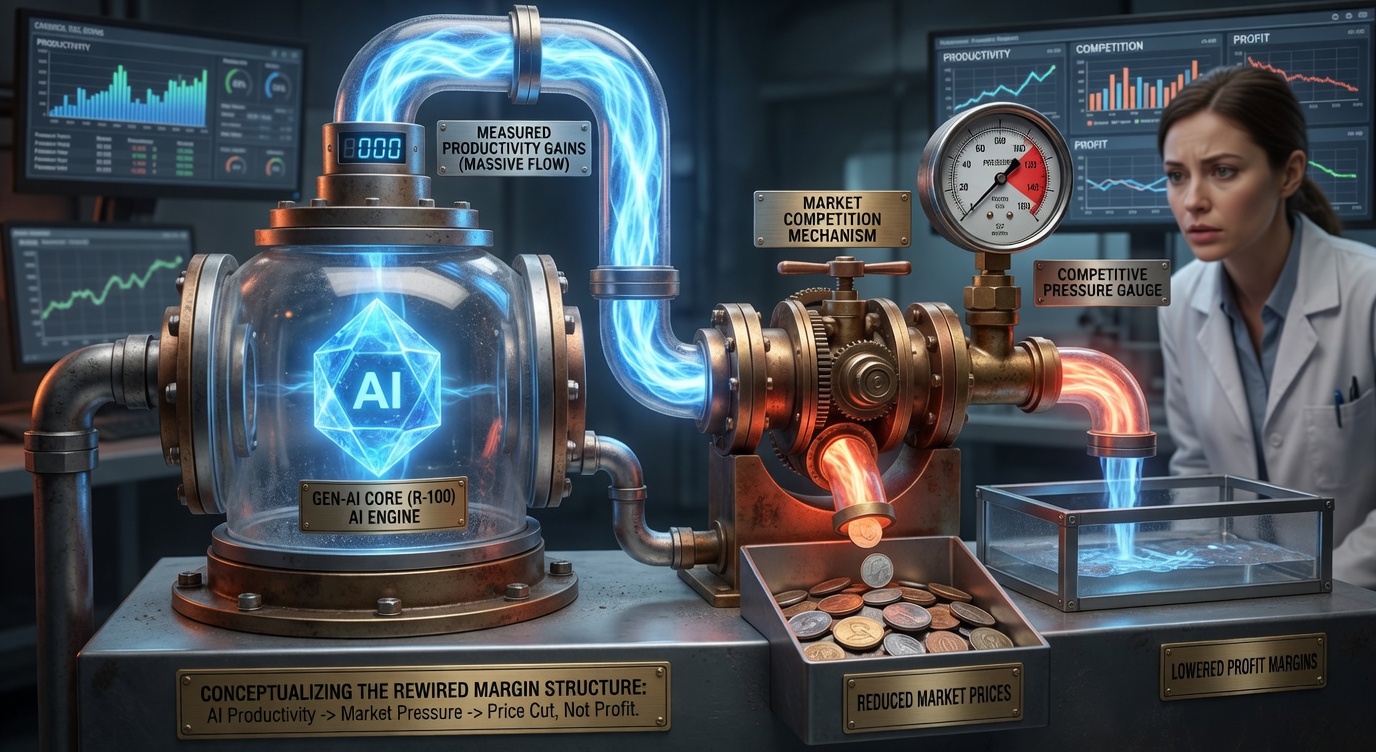

Undoubtedly, the explanation is both simple and unsettling. Essentially, generative AI is mathematically restructuring profit margins. Moreover, it uses algorithms to optimize costs, pricing, and revenue allocation in real time. However, this restructuring can either widen or compress margins. Ultimately, the outcome depends entirely on how the technology is deployed.

For example, firms that treat AI as a faster way to execute existing tasks are seeing efficiency gains competed away. Conversely, firms using AI to re-architect value chains are capturing durable margin expansion.

As management thinker Peter Drucker famously observed,

“The greatest danger in times of turbulence is not the turbulence; it is to act with yesterday’s logic.” In 2026, the Fortune 500 are learning that lesson in hard financial terms.

The Productivity Paradox: Why Faster Work Isn’t Fatter Margins

Historically, assuming that automating tasks automatically improves profitability has been a massively expensive misconception. Indeed, the BCG Henderson Institute’s research makes this vividly clear. First, researchers mapped job roles to work activities for 800 public firms. Next, they scored each activity’s potential for AI augmentation. Consequently, the data showed a sobering reality. Specifically, “even as companies pour resources into gen AI, the resulting productivity gains appear to be competed away, passed on to customers or suppliers rather than retained by firms.”

Essentially, this is the commoditization trap. Whenever a technology makes a capability universally cheap and accessible, then the economic value created by that capability migrates to other parts of the value chain.

For example, photography once commoditized realistic portraiture. As a result, this shift destroyed the livelihood of portrait painters who simply adopted cameras to work faster. Similarly, generative AI is currently commoditizing routine knowledge work. Undoubtedly, the efficiency gains are real. However, they accrue to customers and suppliers, rather than to the firms deploying the technology.

Additionally, PwC’s 2026 Global CEO Survey corroborates this finding. In fact, only 12% of CEOs reported that AI delivered both cost and revenue benefits. Meanwhile, 56% stated they had seen no significant financial benefit whatsoever. Furthermore, an analysis of Fortune 500 10-K filings is even more telling. Currently, 85% of companies mention AI. Nevertheless, only a handful—primarily AI infrastructure sellers—quantify concrete investment returns.

Therefore, the lesson is clear: efficiency alone is not a strategy. Today, every competitor gains access to the same AI models at roughly the same cost. Indeed, API prices that would have run thousands of dollars in 2023 now cost pennies. As a result, speed becomes table stakes, instead of a differentiator.

Algorithmic Margin Restructuring: The Mathematical Models at Play

Meanwhile, beneath the surface, a far more sophisticated dynamic is unfolding. Clearly, generative AI is not merely automating tasks. Instead, it is enabling mathematical algorithms that dynamically restructure profit margins across entire business models.

Incremental Operating Margin: The Ultimate Efficiency Metric

Presently, leading financial analysts track Incremental Operating Margin (IOM) as the definitive measure of AI’s economic impact. Specifically, this metric answers a brutal question. Namely, for every dollar of new AI investment, how much flows to operating profit? Conversely, how much is consumed by compute costs, power, and R&D?

Currently, in 2026, the average IOM for hyperscaler AI investments remains below traditional software benchmarks. Consequently, this highlights the capital-intensive nature of the generative AI build-out. Additionally, Morgan Stanley’s Wealth Management division describes the current environment uniquely. Specifically, they call it a “gen-AI-capex-powered reindustrialization renaissance.” Furthermore, this shift is fundamentally different from prior technology waves.

Previously, asset-light software models enjoyed near-zero marginal costs. In contrast, generative AI is a “cash-hungry R&D arms race.” Therefore, in this model, adding users simultaneously adds significant variable costs.

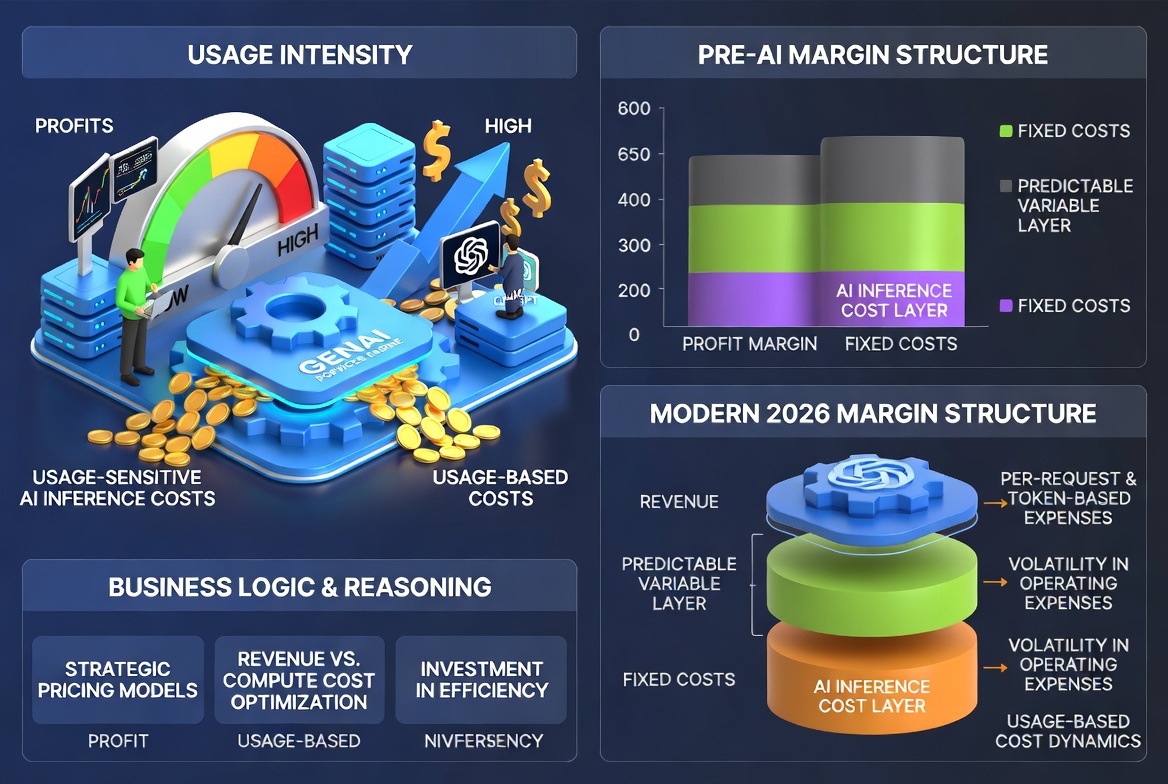

Gross Margin Compression: The New Reality

Similarly, ICONIQ’s 2026 State of AI report reveals a startling statistic. Specifically, surveyed AI product builders expect average gross margins of approximately 52%. Meanwhile, traditional SaaS businesses have long targeted 70–80% margins.

Fundamentally, the reason is structural. Because each AI inference, each agent action, and each prompt triggers real variable costs, these costs post directly into the cost of goods sold. Thus, as one SaaS CFO analyst explicitly warns, “AI COGS behaves more like a usage-sensitive cost layer than traditional software delivery.”

Revenue Decoupling from Labour

Moreover, one of the most profound shifts is the decoupling of revenue growth from headcount growth. Indeed, FTI Consulting identifies this as a primary structural change. Specifically, AI enables organizations to scale revenue without proportional increases in labor. Therefore, it fundamentally alters the operating leverage that has defined corporate profitability for decades.

Ultimately, companies that master this decoupling gain a durable cost advantage. Otherwise, they risk being undercut by competitors whose algorithmic cost structures are permanently lower.

The New Competitive Advantage: Vertical AI Integration

Generally, horizontal AI deployment—like chatbots, copilots, and content generation—produces thin, easily competed-away gains. In contrast, vertical AI integration is where lasting margin expansion materializes.

Embedding AI into Value-Generating Workflows

Accordingly, the GenAI Profitability Paradox framework draws a sharp distinction. Specifically, it states, “If AI does not reshape how revenue is generated or how costs are structured, then the financial impact will remain marginal.”

Instead, vertical AI embeds models directly into critical business processes. For instance, these include sales qualification, claims adjudication, procurement negotiation, order fulfillment, and service dispatch. Ultimately, these are the specific workflows where value is actually created or destroyed.

Indeed, real-world examples are rapidly accumulating. For instance, PwC has deployed ChatGPT Enterprise to more than 100,000 seats. Furthermore, this covers essentially its entire global workforce. Consequently, it is one of the largest corporate AI rollouts in history. Similarly, the Fortune 100 retailer Lowe’s uses AI to generate 3D product models. Because these cost less than $1 each, thus, they contribute to the 37% of retail firms reporting annual cost reductions exceeding 10% through AI.

The Agentic Workforce: 80% of Fortune 500 in Production

Currently, by Q1 2026, more than 80% of Fortune 500 companies are running AI agents in production environments. Furthermore, these agents handle multi-step workflows with limited human supervision. Specifically, use cases range from code generation to customer support and search. In coding, for example, the strongest engineers achieve 10–20× efficiency gains using AI programming tools.

Clearly, the economic impact is measurable. Consequently, organizations deploying AI across core operations report 20–40% productivity gains in year one. Furthermore, top performers are achieving a 10–18× return on investment.

The 74 % Concentration Effect

However, perhaps the most sobering finding comes from recent AI spending studies. Remarkably, 74% of AI-generated returns flow to the top 20% of firms. As a result, the gap between AI leaders and laggards is widening rapidly.

Moreover, early evidence suggests that AI adoption follows a power-law distribution. Under this model, the strongest performers capture disproportionate value. Additionally, AI researcher and Wharton professor Ethan Mollick has noted this pattern of collapsing costs combined with rapidly improving capabilities. Specifically, he states it “is unprecedented in the history of technology adoption.” Therefore, the window for building competitive advantage through AI is narrowing fast.

Conclusion

Ultimately, 2026 marks the definitive shift from AI experimentation to AI profitability. Indeed, the data tells an unambiguous story. First, generative AI can mathematically restructure profit margins for better or worse. However, the outcome depends entirely on strategic deployment.

On one hand, some firms deploy AI vertically. Specifically, they embed it into core value-generating workflows, redesign operating models, and decouple revenue from labor. Consequently, these firms capture durable margin expansion. On the other hand, many firms deploy AI horizontally. Essentially, they simply add chatbots and copilots to existing processes. As a result, they see their efficiency gains competed away to customers and suppliers.

Undoubtedly, the math is unforgiving, yet it is abundantly clear. Furthermore, enterprise AI spending is projected to reach $11.6 million per firm in 2026. Simultaneously, boards are shortening ROI timelines from years to quarters. Therefore, the era of “let’s try AI” is definitively over. Finally, as the Flevy GenAI Profitability Paradox framework concludes, “executives must decide whether GenAI remains a productivity enhancer or becomes operating infrastructure.”

In finding, the question facing every Fortune 500 leader in 2026 is no longer whether to invest in AI. Because that decision has already been made. Instead, the real question is whether their AI investments are structurally improving margins. Otherwise, they are merely helping firms run faster on a treadmill that someone else controls.

FAQs

Is generative AI actually improving Fortune 500 profit margins?

The evidence is mixed. While 92 % of Fortune 500 firms use ChatGPT and AI productivity gains are widely reported, only 12 % of CEOs say AI has delivered both cost and revenue benefits. The key differentiator is whether AI is deployed vertically (embedded in core workflows) or horizontally (as a general productivity layer).

What is the Incremental Operating Margin (IOM) for AI?

IOM measures how much of each new dollar of AI investment converts to operating profit. In 2026, IOM for hyperscaler AI investments remains below traditional software benchmarks due to high compute, energy, and R&D costs.

How are algorithms restructuring profit margins?

AI algorithms dynamically optimize pricing, cost allocation, and revenue models by analysing vast datasets in real time. They enable revenue scaling without proportional labour cost increases, fundamentally altering operating leverage.

What regulations govern AI deployment in enterprises?

Key regulatory frameworks include the EU AI Act (fully applicable from August 2026), Japan’s AI Act, and FINRA’s 2026 guidance on AI governance for financial firms. These regulations impose transparency, risk management, and human oversight obligations.

What percentage of Fortune 500 firms have AI agents in production?

Over 80 % of Fortune 500 companies run AI agents in production environments as of Q1 2026, handling multi‑step workflows from coding to customer service.

References

-

BCG Henderson Institute. Look for New Ways to Create Value When Deploying Gen AI. Boston: BCG, 2026. Available at: https://bcghendersoninstitute.com

-

McKinsey & Company. 生成式AI在中国:2万亿美元的经济价值. Shanghai: McKinsey, 2026. Available at: https://www.mckinsey.com.cn

-

a16z. Thirty Percent of Fortune 500 Companies Have Already Paid for AI. Menlo Park: Andreessen Horowitz, 2026. Available at: https://www.aicoin.com

-

ICONIQ Capital. State of AI: Bi‑Annual Snapshot Report. San Francisco: ICONIQ, 2026.

-

European Union. *Regulation (EU) 2024/1689 of the European Parliament and of the Council laying down harmonised rules on artificial intelligence (Artificial Intelligence Act).* Official Journal of the European Union, 2024. Available at: https://eur-lex.europa.eu

-

Japan. Act on the Promotion of Research, Development and Utilization of AI‑Related Technologies (AI Act). Tokyo: Government of Japan, 2025.

-

FINRA. 2026 FINRA Annual Regulatory Oversight Report. Washington, D.C.: Financial Industry Regulatory Authority, 2025. Available at: https://www.finra.org

-

PwC. 2026 Global CEO Survey. London: PricewaterhouseCoopers, 2026. Available at: https://www.pwc.com